Alberta fed cattle prices have come under pressure over the past month. Alberta packers were buying fed cattle in the range of $147 to $149 during the second week of November, down $4 to $6 from a month earlier. Weakness in the fed cattle market has spilled over into the feeder complex. Western Canadian yearling prices have dropped nearly $15 from the October highs while calves are down $10 to $12.

It’s that time of year when I like to discuss the market outlook for 2019. We’re going to see some major changes in the fundamental structure of the market and producers need to be mindful of the upcoming risks. This will help them plan their marketing or risk-management strategy. We all know that the cattle market is unique every year and 2019 will be no exception.

Read Also

India likely to triple lentil import duty

Analysts anticipate India hiking duties to 30 per cent after March 31 to bolster domestic prices on expectation of strong harvest.

The 2018 U.S. calf crop is estimated to finish near 36.5 million head, up from the 2017 output of 35.8 million head. The 2018 Canadian calf crop is expected to finish near 4.40 million head, up from 4.36 million head in 2017. This will be the fourth year of herd expansion in the U.S. To put this number in perspective, we haven’t seen a calf crop of this size since 2007. Year-to-date Canadian exports of feeder cattle to the U.S. for the week ending Oct. 27 were 170,383 head, up 59 per cent from year-ago levels. U.S. demand has been a major factor supporting domestic feeder cattle prices. However, given the year-over-year increase in the U.S. calf crop, it’s unlikely this pace will continue in 2019. Look for lower feeder cattle exports to the U.S during 2019.

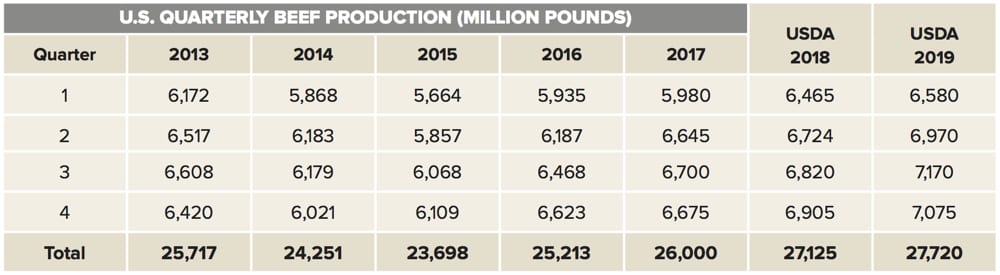

Production increases forecast

A larger calf crop will result in larger feedlot placements, which means a year-over-year increase in beef production. The quarterly beef production estimates from the USDA show a surge in supplies during the second and third quarters of 2019 compared to 2018. Beef exports are also expected to increase but not at the same pace; therefore the domestic market will function to encourage demand through lower prices.

The personal and corporate U.S. tax cuts resulted in a sharp year-over-year increase in consumer spending. U.S. consumer confidence has been hovering near record highs while unemployment levels in Canada and the U.S. are near historical lows. U.S. and Canadian wages are also up about 2.5 per cent from year-ago levels. U.S. grocery store spending has been running four to five per cent above 2017 while spending at restaurants and other eating-out places is up 10 per cent over last year. This demand scenario helped sustain fed and feeder cattle prices during 2018, but this is not sustainable longer term. U.S consumer spending is expected to slow in 2019, which will result in lower beef demand. At this stage, we can expect 2019 U.S. beef demand to be similar to 2018, but don’t count on an increase.

The function of the cattle market is to discourage production and encourage demand through lower prices. I’m expecting feeder cattle prices to trend lower for the first half of 2019.

Cow-calf producers and backgrounders should have a risk-management strategy in place to limit the downside. By the end of 2019, I’m expecting to see a sharp year-over-year increase in the U.S. cow slaughter. Fed cattle prices tend to make a seasonal high in late February or early March which may sustain the feeder market in the first couple of months of 2019.

The 2019 second-quarter beef production is projected to be up nearly 400 million pounds over the first quarter. Domestic beef demand is rather inelastic in a normal year so a sharp rise in supplies can have detrimental effects on the price. Feedlot margins are expected to move into negative territory from May forward which will lower their buying ideas for replacements.