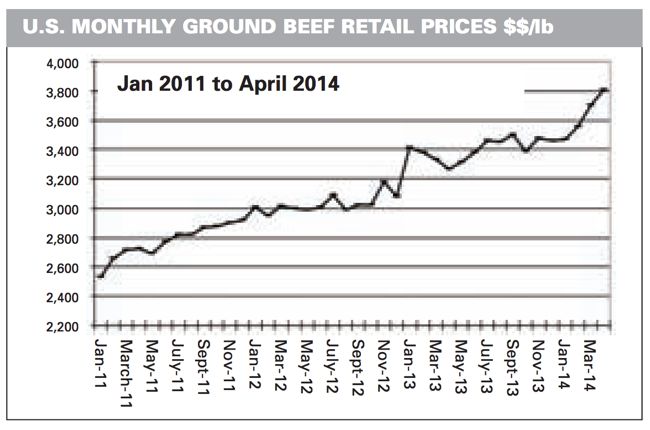

Retail beef prices have surged higher since January, resulting in softer beef consumption. Average American at-home and away-from-home food expenditures were running four and three per cent, respectively, above year-ago levels earlier in 2014. But since March, at-home food spending is now below year-ago levels by two per cent while away-from-home food spending is down 8.4 per cent.

Beef prices are now at levels where the market is rationing demand as disposable income has not increased at the same pace as the beef market. U.S. beef production and feedlot inventories continue to run below year-ago levels, which has resulted in the sharply higher fed cattle prices.

Read Also

Get ready for an eventual transition on cattle traceability

When new federal cattle traceability rules do ultimately take effect, reporting requirements will vary for producers, transporters, feedlots and markets — but most of the onus will be on producers.

Feedlots in Alberta and Saskatchewan continue to experience healthy margins resulting in record-high prices for feeder cattle and cow calf pairs. Feedlot operators in Western Canada have been aggressive sellers into the higher price structure while carrying inventories eight to 10 per cent above year-ago levels. The main question moving forward is how long is this upward trend in the cattle and beef complex going to continue and what are the signals to watch moving forward.

The overall economy has experienced slow growth, which is actually a positive signal that beef demand will remain relatively constant. The U.S. unemployment rate stood at 6.3 per cent in April and 25 states reported the rate under six per cent. There are now 145.7 million Americans working compared to 143.5 during April of 2013. This is a huge factor for the beef complex as income levels increase for the 2.2 million Americans. Consumer confidence continues to grow, reaching a rating of 82 for 2014 which compares to an average rating of 72 from 2008 through 2013. Over the next year, consumer confidence is expected to strengthen to a level of 90, which will be a signal the economy is once again firing on all cylinders. Equity markets have been trading near historical highs and with consumer spending slowly increasing, the financial markets are expected to remain in expansion mode.

U.S. wholesale beef prices have softened since spring. U.S. Choice product levels touched $240/cwt earlier in March but are currently trading near $225/cwt. U.S. beef production tends to increase in the summer, resulting in weaker tone for the wholesale market.

U.S cattle on feed for slaughter as of May 1 were down one per cent from year-ago levels while April placements were down five per cent from April of 2013. The USDA marginally increased their beef production estimate for the second quarter while lowering projections for the third and fourth quarter of 2014.

- From the Canadian Cattlemen: Feeder cattle market looking forward

While the nearby live cattle futures have levelled off, the deferred futures remain in an upward trend. The U.S. year-to-date beef production is actually running 5.6 per cent below year-ago levels for the week ending May 16. Second quarter pork production was also fine tuned higher while marginally lowering the third and fourth quarter numbers.

Alberta and Saskatchewan feedlot inventories continue to run eight to 10 per cent above last year. The Canadian year-to-date slaughter for the week ending May 10 was up four per cent while the total beef output was only up one per cent.

While feedlot inventories are higher, feeder cattle exports to the U.S. are running 43 per cent above last year. This is interesting as it appears that there are more feeder cattle coming on the market sooner, which may result in a tighter available feeder cattle supplies later in the year. For the week ending May 3, year-to-date exports of steers and heifers for slaughter (to the U.S.) were up only one per cent over last year. It appears that fed cattle exports have slowed now that U.S. beef production is increasing relative to the first quarter. However, exports of fresh/chilled cuts continue to come in above last year keeping the Canadian retail supplies at a constant supply.

The fed cattle market is expected to remain relatively stable at the economy continues to expand and consumer spending remains constant into the summer months. Seasonally, fed cattle prices drift lower in the second quarter but the lower supply situation and stable retail price structure should limit the downside.

Alberta break-even prices for pen closeouts during late summer and early fall are forecasted at $144/cwt while current fed cattle prices are near $148/cwt. During May, barley prices have surged, reaching $225 delivered Lethbridge from under $200/mt earlier in April. The cost per pound gain will increase for the summer and fall fed cattle. Western Canadian barley acres are expected to be down 10 per cent from 2013 and the year-over-year increase in domestic feed usage has lowered the ending stocks projection. Feeder cattle prices could run into resistance as the feeding margin structure moves to break even.