Last year I described my “Titanium Strength Model Portfolio,” based on buying and holding strong stocks. Now it’s time to take a look at my results. How did the portfolio perform? How did it compare to market indices? What other nuggets can we glean that might aid our understanding of portfolio management? What does a bell curve have to do with it?

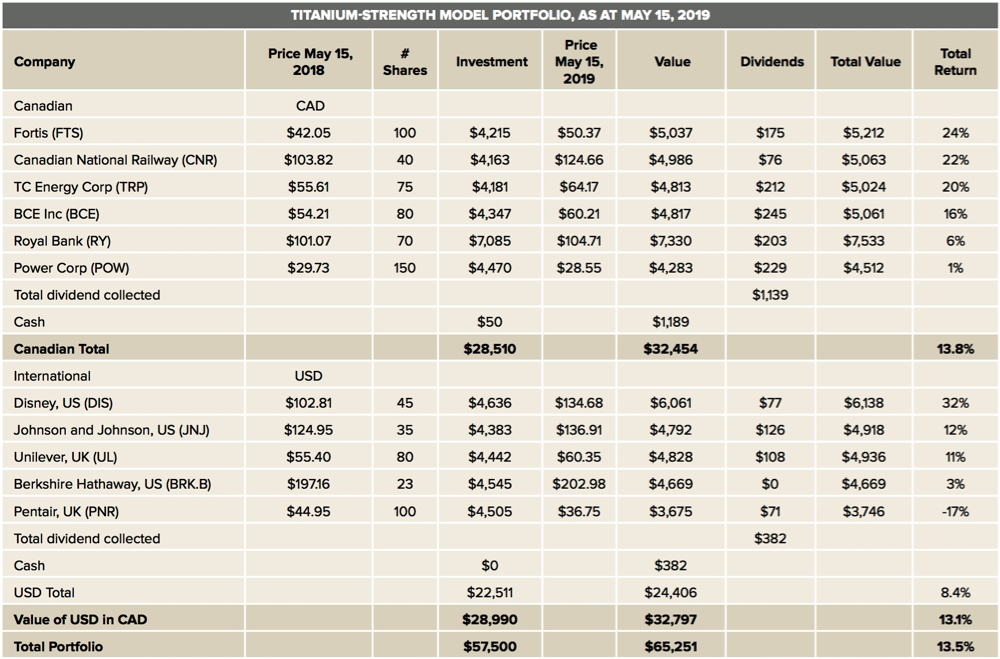

Overall performance was a 13.5 per cent return, pretty good in nominal terms and outstanding compared to market performance, which came in at 4.0 per cent as a weighted average of the Canadian, U.S. and UK markets, including dividends. The international component had a price return of 6.8 per cent and a dividend yield of 1.7 per cent for a total return of 8.4 per cent in U.S. dollar terms. The Canadian dollar also depreciated, making the gain 13.1 per cent in Canadian dollars on the international side.

Read Also

Is the technology in our vehicles a help or a hindrance?

Not only does new tech allow people to operate vehicles and farm machinery with fewer skills, it also creates more problems for vehicle users when those systems fail, Scott Garvey writes.

This is a model portfolio, designed to be simple to understand and show in a chart. In real life, I would further increase portfolio returns by re-investing dividends during the year rather than holding cash.

Outcomes of disciplines that entail variability, like investing or farming, will be governed by the rules of a normal distribution curve, a.k.a. the bell curve. Some returns will be very high, some will be very low, but most will be clustered around the average. While overall performance was outstanding for the year, there is a distinct difference among companies. Disney (with a 32 per cent profit) and Pentair (a 17 per cent loss) represent the outliers of the bell curve. Other stocks in the portfolio came in closer to the average. This portfolio is too small to create a perfect bell curve, but is large enough to demonstrate the concept.

Stratification of individual company performance will always occur. Better portfolios will have better overall performance but will always have a laggard or two and a star or two, with most companies falling near the average.

Many portfolio managers would sell Disney because of its great performance, thinking they should take profits. Many think if a stock moves up by 20 per cent it should automatically be sold, succumbing to the misperception that you need to sell to make money. Other managers would sell Pentair as they “pull the weeds” from the portfolio. However, the only real reason to sell stocks in either company is if their business prospects deteriorate significantly or their valuation becomes unreasonable.

If we sold these two companies and picked two others the portfolio would still be governed by the bell curve, and a year from now we would likely have another outlier on both the good and bad side. Which company will be next year’s star? Which will be the laggard? There is no way to predict this. The only prediction is that a well-structured portfolio of good companies will appreciate in value better than the market average of about 10 per cent per year.

With this demonstration, I hope to illustrate the relative ease of investing in stocks and deriving adequate returns with minimal effort. It took me a long time to realize how simple it is, because virtually everything you read will tell you how difficult it is. Business schools teach students that it’s impossible to beat the market based on a theory called the “efficient market hypothesis,” and most investors only derive half the returns of the market. Charlie Munger, Buffett’s right-hand man for half a century once said, “More investors don’t copy our model because our model is too simple. Most people believe you can’t be an expert if it’s too simple.”

This portfolio is similar to the process I take with my newsletter, where I provide TFSA and RRSP model portfolios, and an actual non-registered portfolio.