Options are considered one of the riskiest investment instruments. Googling “options” can result in some pretty terrifying descriptions like “The price of options can change quickly, and those who trade them can win or lose huge sums of money in very short periods of time. This type of trading is best left to professionals,” or “The options arena is not to be treaded lightly and not by novices,” and, more succinctly, “They are basically gambling instruments.”

- Read more: How I doubled my money in less than four years, Part 1

- Read more: How I doubled my money in less than four years, Part 2

Read Also

Is the technology in our vehicles a help or a hindrance?

Not only does new tech allow people to operate vehicles and farm machinery with fewer skills, it also creates more problems for vehicle users when those systems fail, Scott Garvey writes.

These descriptions can be correct given the propensity of people to think and act on a short-term basis. However, in the hands of a long-term investor, options can be used to enhance performance and even reduce risk. My options strategy revolves around the sale of puts, representing about 90 per cent of my option trades.

If you like a company and thought the current price was fair, would you be even happier getting a 10 to 20 per cent discount? This can be realized by initially selling puts. I have learned through the ultimate educational institution, “The School of Hard Knocks,” to only sell puts on larger companies that are reputable and financially sound. Luckily, such companies have the most liquid options with available expiring dates up to two and a half years into the future.

An article cannot provide complete education on options and given most of my activity is the sale of puts, I will describe them briefly. A put is the right but not the obligation to sell a stock at a certain price, called the strike price, on or before a certain date in the future — the expiry date. When I sell a put, the buyer is purchasing the right to sell me the stock. Option pricing is set by open auction, just like stocks. Their price movement is related to the underlying stock price movement but is also independent of it. That might sound like a lot of mumbo jumbo so let me illustrate with a real-life example.

Real-life example

On October 31, 2019, I sold one put contract on well-known 3M. The put has a strike price of $180, expiring on January 21, 2022, about 27 months into the future. I received $33.20 per share or $3,320 less fees for the 100-share contract.

The buyer paid me $3,320 for the right to sell me 100 shares of 3M at $180 per share any time up to January 21, 2022. If he exercises his right, my effective cost is the strike price of $180 minus the $33.20 proceeds from the put sale, equaling $146.80 per share. At the time of the put transaction, 3M was trading at $166.27, making my effective purchase price 12 per cent less than the then price of 3M.

The following scenarios could play out:

- 3M rises in value and exceeds $180 at expiry. This is my most desired outcome as I would get to keep the $3,320. The purchaser of the put wouldn’t sell me the stock for $180 if it was worth more.

- The price ranges between $180 and $146.80 at expiry. While the purchaser of the put can sell me the stock anytime, this rarely occurs until just before expiration. If the price of 3M is in this range, I can either buy back the contract profitably or allow the stock to get put (sold) to me. As expiration approaches the value of the put approaches the differential between the strike price and the stock price. If 3M was at $170 near expiration, the put would be valued around $10 and I could buy back the contract earning almost $23.20, having invested nothing.

- The price declines below $146.80. In this case, I could buy out the contract at a loss or have the stock put to me. If 3M dropped to $120, I would have to pay about $60 to buy it out (strike price minus current price) and would lose $26.80 per share. This sounds bad but if I bought the stock on the same date as selling the put, I would have experienced a paper loss of $46.27, significantly more than my loss selling the put. In these situations, I rarely buy out, thus accepting the stock in anticipation of a recovery. That’s why put selling works best on solid companies, where risk of permanent loss is minimal.

Currently, with about six months to expiry, 3M is at $203 and the option is valued at about $6. I could buy it out, but generally wait for expiration. If it stays above $180, I will pay nothing and keep the $3,320. Cool, eh!

Switching gears

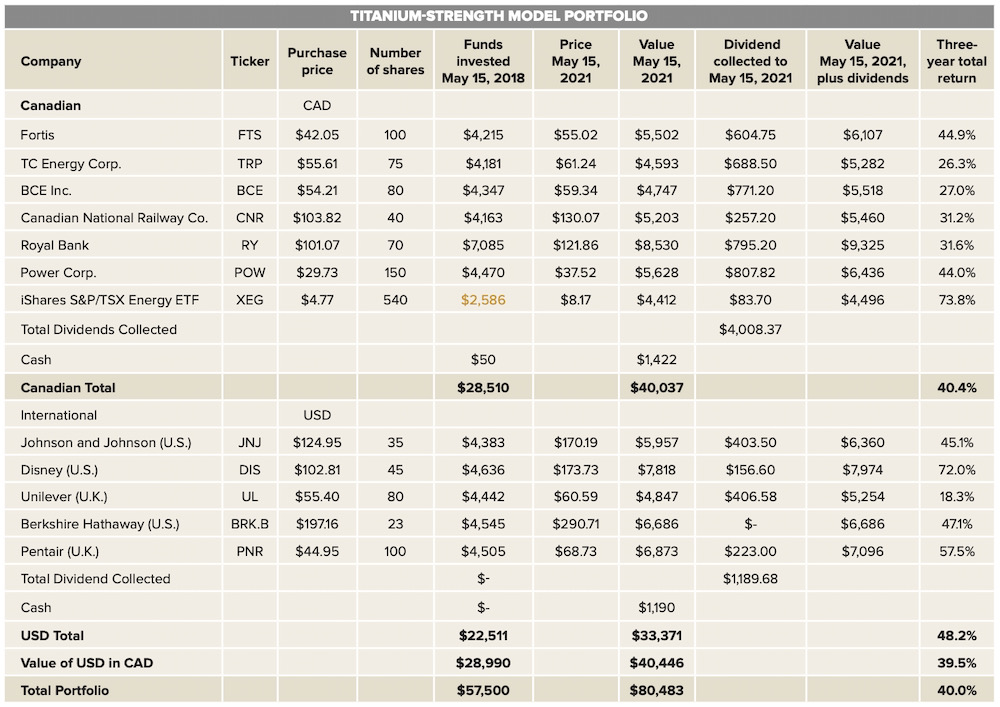

The Titanium Strength Portfolio celebrated its third birthday on May 15. As this is my first article written since then, an update is appropriate. On its birthday the TSP was worth $80,483, up exactly 40 per cent and nicely ahead of my long-term goal of 10 per cent per year.