The cattle market has been very difficult to analyze over the past seven months.

There are three main challenges. First, the recent market behaviour has been unprecedented. There are no past examples to compare the current environment. For example, the United States weekly slaughter decreased from April through June. This was the first time in modern history that this occurred.

U.S. dressed weights are about 20 pounds higher than last year and 40 pounds heavier than the same period of 2023.

Read Also

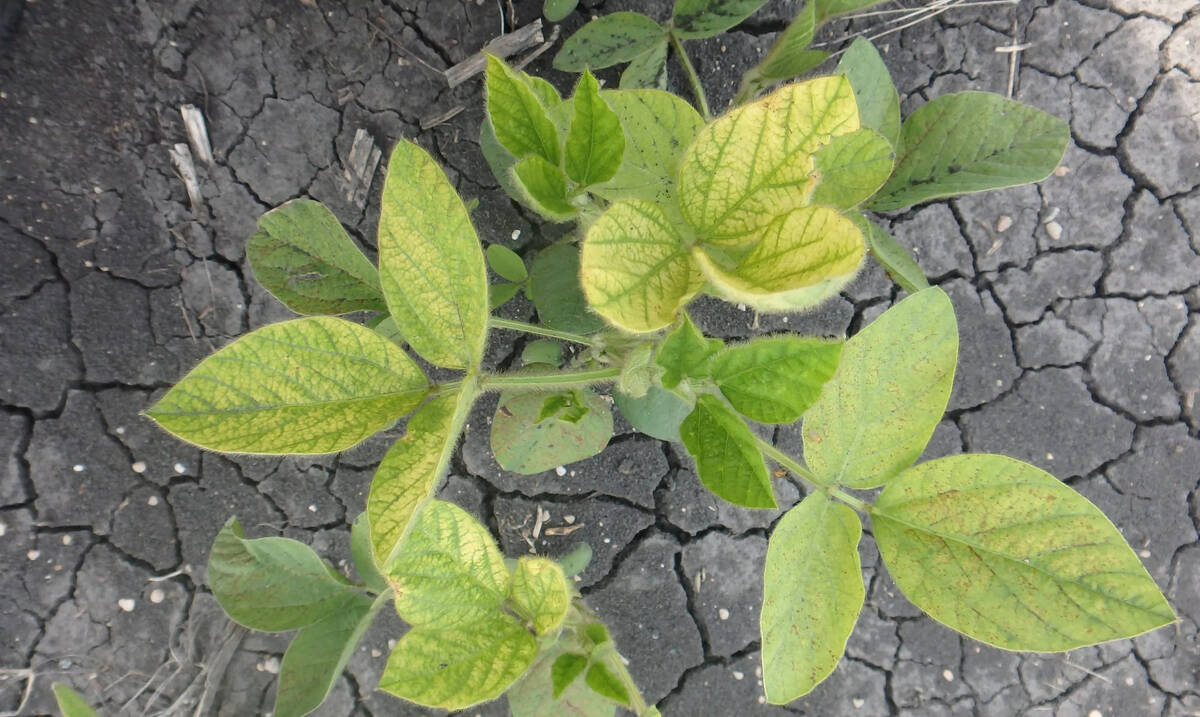

Selecting IDC-tolerant soybeans doesn’t reduce yield, Manitoba study confirms

University of Manitoba research shows soybean varieties selected for iron deficiency chlorosis (IDC) tolerance protect yield in affected areas without reducing performance elsewhere in the field.

Secondly, economic theory has not held water. Retail beef prices are at historical highs. Higher prices usually result in less demand. In my recent discussions with an analyst from south of the border, he stated that there is a strong argument that consumer demand has actually increased.

Finally, cattle producers and analysts have been basing decisions on U.S. government policy. The problem is that U.S. government policy has been changing.

During the first week of July, Alberta packers were buying fed cattle in the range of $295-298 per hundredweight FOB feedlot in southern Alberta. Prices are steady to $3 per cwt. compared to 30 days earlier. In Kansas, fed cattle prices were quoted at US$224-225 per cwt., down US$7-8 per cwt. from the first week of June. U.S. wholesale choice beef was valued at US$395 per cwt., relatively unchanged from a month earlier. The rally in the fed cattle market and wholesale beef complex appears to be stalling.

Cattle on feed 150 days or more are above year-ago levels on both sides of the border. In the U.S., cattle on feed 150 days or more as of June 1 were 3.013 million head, up 253,000 head from 2024. U.S. cattle on feed 180 days or more as of June 1 were 1.430 million head, up 308,000 head or 27 per cent from last year. For the week ending June 28, U.S. dressed weights were averaging 865 lb., up 24 lb. from last year. Despite the larger fed cattle supplies and heavier weights, the U.S. weekly slaughter for the week ending June 28 was 560,000 head, down 50,000 head compared to the same week of 2024.

In Alberta and Saskatchewan, cattle on feed 150 days or more as of June 1 were 359,177 head, up 2.9 per cent or 9,957 head from the June 1, 2024, number of 349,220. Dressed weights in Western Canada are similar to year-ago levels.

Feedlots appear to be current with production.

Beef demand appears to be significantly stronger than earlier anticipated. U.S. restaurant traffic during June was running eight to 12 per cent above year-ago levels. Canadian restaurant visits during June were up a whopping 20 to 24 per cent compared to June 2024. Restaurant spending in both Canada and the U.S. has been up five to seven per cent from year-ago levels. Consumer spending at grocery stores has been running three to four per cent above 2024.

In the U.S., there appears to be a change of tastes. There is a fad or trend to increase protein intake to trim the waistline. For example, in the U.S., Subway restaurants had an advertisement: “Come to Subway for your protein.” The “carnivore diet” is also taking hold amongst certain demographics.

Average U.S. ground beef prices are up 16 per cent from year-ago levels. Prices for boneless sirloin steaks are up five to six per cent compared to June 2024. Beef is often used as a loss leader for grocery chains. The beef counter is at the back of the store, similar to milk and eggs, and customers often have to wait for service. The longer a customer is in a grocery store, the more they spend. When I checked random flyers in the U.S. Midwest, there were significant discounts for steaks over special holidays such as Father’s Day. One flyer had steaks 30 to 50 per cent off regular price. The North American consumer may not be experiencing the full effect of the year-over-year increase in beef prices.

Feeder cattle prices have mirrored the fed market. Western Canadian auction markets generally take summer holidays during June and July. Cow-calf producers have sold a record number of calves and yearlings for fall delivery. At the time of writing, 1,000-lb. steers for September and October delivery were trading in the range of $395-400 per cwt. in central Alberta and Saskatchewan. Quality genetic steer calves averaging 650 lb. for October and November delivery have been quoted at $550 per cwt. FOB farm in Alberta. Angus-cross steers with a base weight of 550 lb. were valued at $585 per cwt FOB farm for early November delivery in southern Alberta.

A steer purchased for 1,000 lb. in August has a break-even fed cattle price for November or December delivery $332 per cwt. The break even for feed costs only is around $320 per cwt. The December live cattle futures were trading at US$208 per cwt., which equates to a Alberta live price of $282 per cwt. Replacement cattle purchased for August and September delivery are too high priced for the feedlot to be profitable. For this reason, I’ve been advising cow-calf producers to sell at least 50 per cent of their expected marketings for fall delivery.

The industry is expecting Canadian and U.S. cow-calf producers to retain heifers this summer and fall for herd expansion. The extent of heifer retention is a wild card. Some analysts in the U.S. don’t believe it will be as significant as earlier anticipated. In Canada, our straw-poll survey suggests that 30,000 to 40,000 heifers will be held back for herd building in the latter half of 2025.

Analyzing the cattle market and price forecasting have been very difficult this year. While hindsight is easy, we can all appreciate the task at hand.